Why Tech Won't Decide DPP Winners—Platforms and Politics Will

How Marketplaces and Geopolitics Will Shape the Digital Product Passport Market

Digital product passports are on the way. More companies are developing DPP solutions, and others are setting up DPP pilots and deployment plans, mainly for 2025-2026 to meet the 2027 requirements.

Many believe that as DPP providers compete, the best technology will win out. This technology needs to be able to scale well, be secure, work with other systems, and be affordable. As the market drives the adoption of DPPs, buyers and sellers will choose the best solutions, showing which ones succeed and which ones don't.

However, the success of DPPs will not be determined by technology alone. The actual outcome will be different from what's expected, as the market is also shaped by platform dynamics and geopolitics, alongside competition between technologies.

This article explains how the DPP market will evolve using a three-layer approach.

First, let's consider the potential size of the market.

Market Outlook

Forecasts for the DPP market vary due to regulatory uncertainties, but they all project rapid growth from a base of $183-338 million in 2024/2025. By 2030, estimates range from $1.2 billion to $5.4 billion, with the potential to reach $7-$10 billion by 2035.1

A range of sectors is expected to drive this growth. For example, the market for DPPs in batteries was valued at $3.4 million in 2024 and is expected to grow to $36 million by 2031, at a compound annual growth rate (CAGR) of 40.6%.2 The electronics sector, including smartphones, laptops, and appliances, is expected to be worth $936 million in 2025 and could rise to $695 million to $2.1 billion by 2030.3

Estimates have also been made regarding the number of DPPs what could be potentially issues. An estimate of for the apparel and textiles sector found that over 62.5 billion could be issued globally by 2030.4 Across all sectors, as many as 540 billion DPPs could be issued by 2030 assuming USD 0.01-0.10 per DPP against market forecasts.

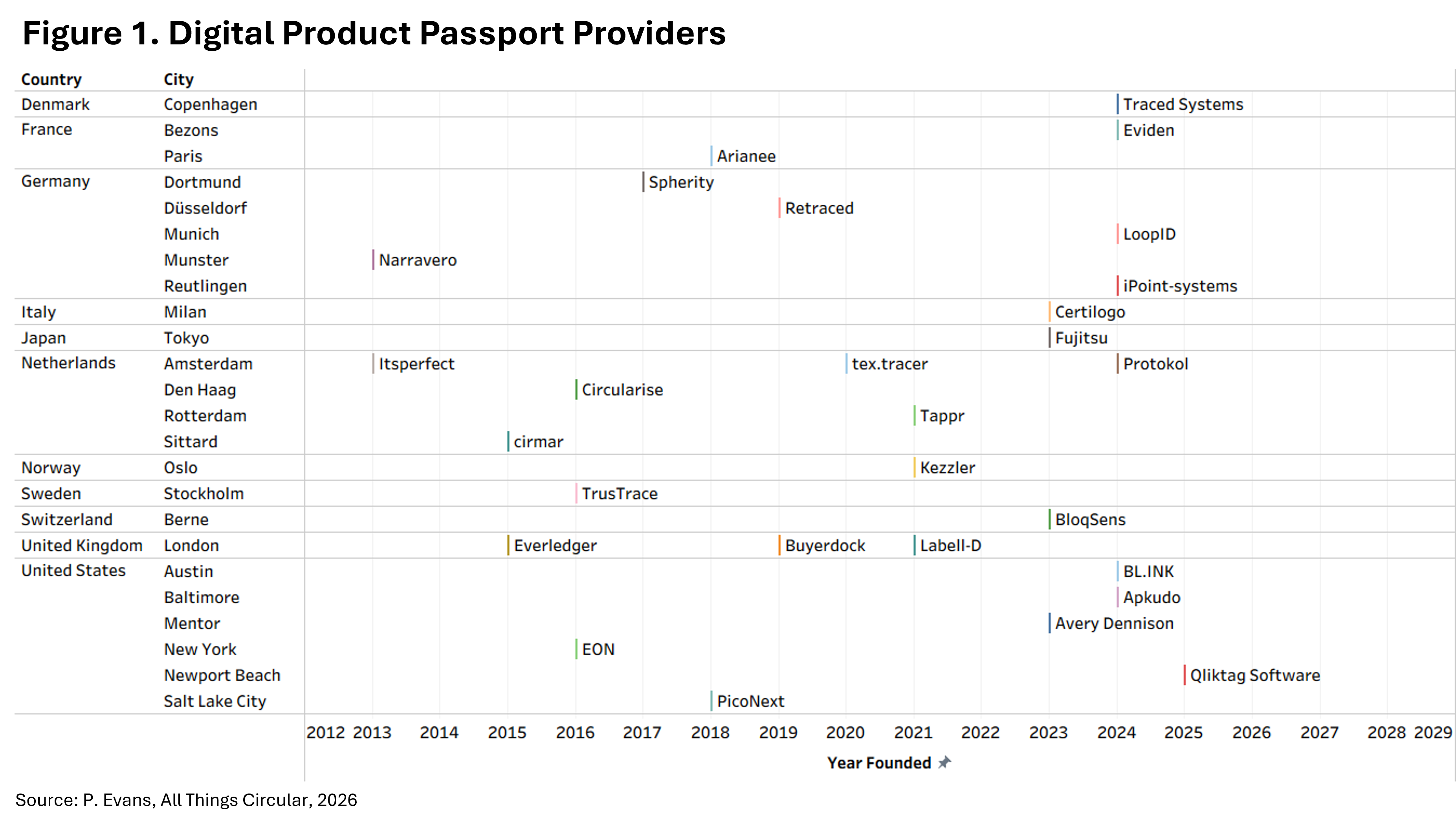

These forecasts are attracting companies to enter the market, with over 30 providers now offering commercial products (see Figure 1 for some of the companies). The DPP market is expected to continue growing rapidly, with some sectors experiencing particularly high growth rates. For example, the electronics sector is expected to account for around 39% of the total market by 2030, with a CAGR of around 40%.

The rush is clearly on. Twelve of these offerings have been launched since 2023.

DPP providers coalesce into six archetypes, each leveraging distinct tech stacks.

Main DPP Types

Blockchain/DLT Specialists (Circularise, Everledger, Retraced): Emphasize decentralized, tamper-proof traceability for supply chains.

Physical ID/Tag Providers (Avery Dennison, Kezzler, Qliktag): Supply NFC/QR hardware linked to digital records.

Luxury/Digital ID Platforms (Arianee, EON): Focus on authenticity/certification for high-value goods like fashion.

ERP/Enterprise Integrators (Fujitsu, Eviden, iPoint-systems): Embed DPPs in PLM/PIM for OEM compliance.

SaaS/Compliance Platforms (BloqSens, Certilogo, Spherity, TrusTrace): Offer end-to-end lifecycle management, often battery/textile-specific.

Emerging Specialists (Apkudo, BL.INK, Buyerdock, cirmar, Itsperfect, Labell-D, LoopID, Narravero, PicoNext, Protokol, Renoon, Tappr, TAZAAR, tex.tracer, Traced Systems): Niche tools for electronics, traceability, or circular apps.

Three Layers Shaping DPP Deployment

Conventional wisdom says that technological competition will favor scalable, secure, interoperable, and cost-effective DPPs, and buyer and seller choices will determine the market winners, dictating rollout. We can call this Layer 1. However, there are other important layers to consider. A second layer is the role digital platforms will play, through the listings and transactions they support. We can call this Layer 2. Another factor is geopolitics, which will shape the establishment of standards and policies. We can think of this as Layer 3.

Let’s look at each of these layers one by one.

Layer 1: Technology Competition

Digital Product Passports (DPPs) bring together different technologies to create a complete data ecosystem for a digital rendering of a product’s lifecycle. This leads to strong competition and innovation in areas like data storage, access, analysis, and cybersecurity. The key technologies used include unique identifiers like QR codes, NFC/RFID tags, and barcodes.5 These identifiers link physical products to digital records that contain 50-100+ attributes, such as information on materials, carbon footprints, origins, repairability, and recyclability.

Other technologies used include blockchain/DLT for secure data sharing, PLM/PIM/ERP systems for data collection, IoT/digital twins for real-time updates, and AI/ML for predictive insights like maintenance forecasting. To protect sensitive supply chain data, robust cybersecurity protocols are used, including zero-trust architectures and end-to-end encryption.6

The technology competition involves different DPP models based on their scalability, access, trust, and integration. Companies like Circularise, which specialize in blockchain, emphasize the importance of decentralized and unchangeable data for supply chain verification. However, they face challenges with speed and costs compared to ERP integrators like Fujitsu, whose DPPs embedded in PLM systems can collect OEM data smoothly but lack the consumer-facing aspect of physical IDs from leaders like Avery Dennison, known for durable tags, or Kezzler, known for dynamic QR codes.

SaaS platforms like Certilogo excel in pilots for batteries and textiles with flexible APIs, surpassing luxury ID providers like Arianee, which focus on branded resale, in terms of broad compliance. Meanwhile, new tools like Apkudo innovate in specific areas like electronics but lag behind in terms of interoperability and application scope.

Layer 2: Platform Dynamics

Platforms will play a crucial role in a second layer of competition for DPP deployment. As economic operators, online marketplaces like Amazon, eBay, and Temu must comply with EU DPP regulations when dealing with regulated goods like batteries, textiles, and electronics. This requires them to check that products meet ecodesign, safety, and traceability standards before listing, using DPPs provided through QR codes, APIs, or carriers. They also need to reject non-compliant items, give consumers easy access to product information, monitor high-risk categories, and report any violations, which can lead to fines of up to 6% of their global revenue.

To meet these requirements, platforms will have to adjust their infrastructure to support DPP creation, storage, and management. This includes making sure their systems can register unique product and operator identifiers in the EU DPP Registry and interact with its web portal, which serves as the central reference for product identifiers, mandatory metadata, and access rights.7 The main challenges are standardizing data, getting accurate and timely information from suppliers, balancing privacy and security, and coordinating operations.

Achieving full compatibility with a large number of providers can be complicated and expensive, so platforms are likely to focus on scalable and verified integrations. They will also accept DPPs that meet industry standards from other providers, like GS1 and QR codes. To ensure compliance, platforms will require sellers to include DPP data and links in their listings and verify their products before approval. Sellers who do not comply risk being removed from the platform.

Instead of integrating with all 30 or more DPP providers, platforms will likely choose a few preferred providers and require sellers to use them through their terms of service. The decisions made by major platforms like Amazon, eBay, and Temu will have significant consequences, as they engage with over 2 million sellers combined. Their choices could shape the market winners, making them important gatekeepers for DPPs.

Layer 3: Geopolitical Rivalry

Geopolitics adds a critical dimension to the evolution of Digital Product Passports (DPPs), as Europe’s regulatory momentum coincides with the erosion of World Trade Organization (WTO) rules. This shift enables “strategic autonomy” tactics that may favor European firms over their U.S. and Chinese counterparts through mechanisms such as data localization, certification biases, and non-tariff barriers.

EU DPP standards—still being finalized through delegated acts—could, for instance, require that product data be stored within EU-based cloud infrastructures subject to GDPR-like adequacy conditions.8 Such rules might benefit European players, echoing France’s steps to favor domestic videoconferencing tools as part of its “digital sovereignty” push. Similarly, the upcoming EU DPP Registry—positioned as a centralized, EU-controlled access gateway—could introduce a “European preference” in access or verification rights, paralleling proposals for public procurement rules that privilege local technology providers.

Harmonized standards established through bodies like CEN and CENELEC for DPP data carriers (e.g., QR codes or NFC chips), data models, and interoperability frameworks could further embed European-centric requirements. Such provisions may be difficult for certain solution providers to meet. In a context marked by renewed U.S. protectionism and potential reciprocal actions under “America First” trade policies, these measures risk shaping the evolution of DPP implementation. DPPs could emerge as instruments of industrial policy. The European Union could leverage “trusted provider” designations to condition market access, force DPP data residency and channel subsidies toward European startups.

Intertwined Dynamics

These layers do not work alone. They are connected. EU regulators have fined US platforms billions of dollars. Apple was fined €500M in 2025 under the DMA, Meta was fined €200M, and Google was fined over €2.95B for antitrust issues. This is due to concerns about gatekeeper abuses and market control in Europe. With over 60 cases of DMA enforcement and concerns about dominance, the DPP could be another way to control antitrust issues and data sovereignty.9

The Brussels Effect will also play a role. This is when EU regulations become global standards because multinational companies adopt them to access the EU’s large market. Instead of having separate compliance systems, companies worldwide follow EU rules.10

This creates barriers that help European companies and set global standards for supply chains, similar to what happened with the General Data Protection Regulation (GDPR). The GDPR controls how personal data is collected, processed, stored, and transferred for EU residents to protect their privacy. It had a big impact on companies outside Europe that offer goods or services to EU residents or track their behavior.11

DPPs could take this further. By requiring unique digital records for products sold in the EU, they would force US software providers and Chinese manufacturers to use EU formats, privacy controls, and environmental metrics globally. This would create barriers that help European companies and set global standards for supply chains.

Conclusion

In summary, technological competition (Layer 1) is unlikely to fully determine DPP deployment. Platforms (Layer 2) and geopolitical maneuvering (Layer 3) will also hold sway. The Brussels Effect will amplify this, exporting EU standards on data residency, privacy, and ESG metrics worldwide, and potentially favoring European DPP providers as the rules-based international trade system comes under pressure.

Companies in batteries/automotive, textiles, and electronics should map DPP readiness across these layers to craft compliant, value-capturing strategies ahead of 2027 mandates.12

Sources