Why eBay Pays Allstate for Circular Insurance: Powering recommerce—but only selectively

How insurance drives network effects in certain categories

Platforms do more than just connect buyers and sellers. They also build trust on a large scale. This is particularly important for recommerce, where trust is a major issue.1 To address this, many platforms now offer warranties on refurbished electronics. This creates strong network effects, where buyers feel more confident and are more likely to make a purchase. As a result, better sellers are attracted and the platform’s variety and liquidity increase. Insurance protects consumers and also drives growth in circular business models.

This approach doesn’t work everywhere, though. It is more effective in some areas of the circular economy than others. This article looks at how and when insurance can help with circular transactions, using the example of eBay and Allstate. We’ll examine why eBay pays Allstate to insure electronics recommerce but probably won’t offer similar coverage for Depop’s peer-to-peer fashion marketplace, which eBay is in the process of acquiring.2

The analysis shows a key pattern: insurance usually supports business-to-business transactions for high-margin products, while peer-to-peer and seller-side activities get less support. This has significant implications for how and where platforms will develop and support circular economy transactions.

Origins of eBay-Allstate Protection Plans

The partnership between eBay and Allstate Protection Plans came about after Allstate acquired SquareTrade, a warranty specialist, in 2017 for $1.4 billion.3 This move positioned Allstate to lead in embedded insurance for online marketplaces. SquareTrade, founded in 1999, was a pioneer in consumer electronics warranties, selling them through major retailers like Costco and Amazon. By 2016, it had serviced millions of devices. In 2020, eBay launched its Certified Refurbished program to grow its electronics resale business.4 eBay needed a way to build trust with buyers beyond just badges and return policies for refurbished items like laptops and phones. This set the stage for the partnership with Allstate.5

The Allstate Protection Plan on eBay covers refurbished and certified open-box products in categories with high mechanical and electrical failure risks, where there is enough data to price coverage accurately.6 These categories include consumer electronics, such as laptops, tablets, smartphones, and gaming consoles. Other categories include small appliances like vacuums and kitchen appliances, select home appliances, refurbished automotive parts on eBay Motors, and audio equipment like home speakers and headphones. The plan offers a 2-year warranty for Certified Refurbished items and a 1-year warranty for items in Excellent, Very Good, or Good condition from professional refurbishers. The protection covers breakdowns, malfunctions, and some accidental damage, with claims handled through eBay receipts and Refurbished badge verification by Allstate. Only top-rated business sellers who meet certain requirements are eligible, and coverage starts automatically at checkout, with no need for buyers to opt in.

A key feature of the eBay Refurbished warranty is that eBay covers the cost of the Allstate protection plan, so buyers don't have to pay extra for it. According to eBay's official Refurbished Warranty page, "this warranty is included at no extra cost with the purchase of an eBay Refurbished product and cannot be bought separately".7 This means the warranty is a standard part of the eBay Refurbished program, not an optional add-on at checkout. eBay pays Allstate to provide the coverage for all eligible refurbished purchases. When someone buys an eligible eBay Refurbished item, eBay automatically shares their email address with Allstate, registering the warranty coverage from the purchase date. This is intended to improve the user experience: the buyer is fully covered without having to choose, pay for, or activate a protection plan.

Other platforms follow eBay’s approach of subsidizing buyer protections to boost recommerce network effects. Some partner with third-party insurance providers, while others self-insure to minimize risk on high-margin electronics. For example, Amazon’s Renewed Guarantee offers 1-2 year warranties on refurbished phones and laptops, absorbing premiums to grow its category, similar to how eBay works with Allstate.8 Back Market, on the other hand, partners with warranty providers like SquareTrade to offer 12-36 month “No Lemon” coverage on certified devices, subsidizing a 50% increase in buyer conversions through embedded insurance.9

Swappie and Reebelo also choose to self-insure. Swappie, based in Finland, provides 12-36 month warranties on all refurbished iPhones, covering technical issues and offering optional Swappie Care for accidental damage.10 Reebelo, headquartered in California, offers 12-month vendor warranties on smartphones, laptops, and tablets, with ReebeloCare extensions for damage from drops and spills.11 All these platforms focus on high-margin, data-rich electronics, where building buyer trust drives supply-side growth, regardless of the insurance model used.

Sellers Get Less

When we examine sellers on platforms, we find they receive significantly less direct insurance coverage than buyers. Allstate provides no direct insurance protection to sellers through eBay’s Protection Plans program, with warranties exclusively indemnifying buyers for post-purchase product failures, while sellers receive only indirect operational benefits from the resulting buyer trust and transaction volume. Sellers gain Certified Refurbished badges that secure top search placement and drive 40%+ sales uplift, top-rated business seller status that unlocks program participation for professional refurbishers to scale, and claims servicing where Allstate coordinates fulfillment “on behalf of” sellers—but bears no financial indemnity as sellers fully cover repair/replacement costs.

Sellers lack product liability coverage for warranty failures, inventory damage protection for stock, business interruption insurance for operational downtime, or legal defense against disputes. As a result, they remain responsible under eBay’s seller agreement for product quality and fulfillment with no premium relief or reinsurance from Allstate.

Platforms strategically prioritize demand-side trust to ignite network effects while positioning sellers as qualified professionals expected to self-insure operational risks. eBay subsidizes generous buyer warranties (Allstate Protection Plans) that slash perceived risk on refurbished electronics and drive 50%+ conversion lifts—but sellers receive only indirect benefits like badges, visibility, and volume. Direct seller coverage would introduce moral hazard (poor refurb quality) and require expensive per-seller underwriting that platforms avoid, ensuring insurance serves as a demand moat rather than supply subsidy.

P2P Transactions Get Even Less

Peer-to-peer (P2P) transactions involve individual consumers directly buying and selling used goods through platforms like Depop, Vinted, or Facebook Marketplace, with no intermediary vetting, quality control, or professional refurbishing—making them the riskiest quadrant for insurers and the recipients of the least coverage, typically limited to basic escrow or tracked shipping reimbursement. Unlike B2B transactions, where platforms like eBay enforce seller standards and provide Allstate warranties, P2P sellers are everyday individuals shipping personal items “as-is” from their closets, leading to uninsurable quality risks where 80% of disputes stem from “not as described” issues like wrong sizes, colors, or undisclosed defects.

This creates a moral hazard nightmare for insurers, as individuals can easily hide flaws in photos and lack repair standards or manufacturer-grade processes, while thin margins on low-value fashion items make warranty premiums uneconomical compared to high-margin phones. Platforms tolerate this risk by funding only escrow services that hold buyer payments until confirmed receipt and transit labels with modest loss caps (e.g., Depop’s £250 maximum), avoiding deeper product liability coverage that would require impossible per-seller underwriting across millions of micro-transactions. eBay’s recent $1.2B Depop acquisition exemplifies this limitation, promising “buyer protection” upgrades that will likely mean enhanced escrow and shipping rather than warranties, confirming P2P’s structural insurance ceiling without breakthroughs like Digital Product Passports or AI authentication to make unvetted inventory insurable.

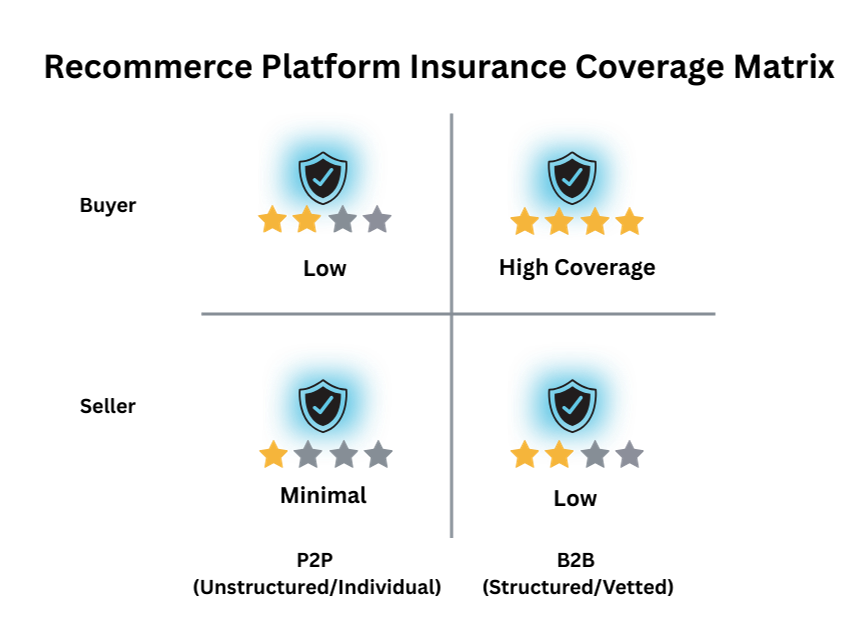

Platform Insurance Matrix

Having established why platforms like eBay pay Allstate for buyer warranties while sellers and P2P transactions receive minimal direct coverage, we can create a 2×2 framework to map and explain these patterns.

B2B Buyer Quadrant: On platforms like eBay, buyers in structured, vetted B2B transactions get high insurance coverage through partnerships like Allstate warranties. This coverage handles defects and quality issues with professional sellers’ inventory. It reduces buyer risk, builds trust, and drives 1.7x network growth by encouraging repeat purchases in high-margin categories like electronics. This is possible because the platform controls seller standards, pricing data, and underwriting.

P2P Buyer Quadrant: In peer-to-peer platforms like Vinted or Depop, buyers get only minimal coverage. This is usually limited to escrow holds and basic shipping reimbursement, like a £250 cap. This is because individual sellers ship “as-is” items, which can have hidden defects and lead to disputes. Poor photo quality and no refurbishing standards also contribute to this issue, making premiums too high for low-value fashion items that cost $20-50 on average. As a result, growth is modest at 1.2x without more comprehensive warranties.

B2B Seller Quadrant: In B2B ecosystems, sellers get indirect benefits like badges, analytics, and sales tools instead of direct coverage. Platforms use the money they would spend on seller warranties to attract buyers and boost sales for vetted sellers. This approach uses structured data to work efficiently but avoids individual policies for each seller. Instead, it relies on collective risk pooling through platform guarantees, creating a flywheel effect without needing separate seller insurance.

P2P Seller Quadrant: P2P sellers get almost no coverage beyond transit labels and face full liability for claims that items are “not as described”. Most disputes, about 80%, come from hidden flaws in personal items. Platforms do not underwrite millions of small transactions, leaving sellers at risk. This limits the growth of P2P markets, creating a ceiling on their potential, unless innovations like Digital Product Passports for authentication are introduced.

Implications

The 2×2 Insurance Coverage Matrix reveals that insurance plays a crucial role in driving growth for circular economy platforms, but largely in the B2B/Buyer quadrant. This is because the structured data and healthy margins in this quadrant enable robust warranties, such as eBay’s partnership with Allstate.

In the B2B sector, high buyer coverage leads to an increase in network effects by reducing perceived risk. This results in repeat purchases of high-value electronics and increased sales for vetted sellers. In contrast, P2P platforms have limited escrow options, which restricts their growth. This limits the scale of these platforms to low-margin fashion resale. The lack of coverage in three quadrants highlights the need for controlled ecosystems, such as those provided by OEMs and aggregators like eBay, to ensure standardized quality.

eBay’s acquisition of Depop for $1.2B, announced on February 17, 2026, and set to close in Q2 2026, brings together Gen Z fashion and eBay’s tools, including Authenticity Guarantee and shipping. However, expanding third-party insurance to P2P is unlikely due to the risks associated with unvetted transactions. Self-insurance would also be costly, with high dispute costs and thin margins, similar to Depop’s £250 escrow limits.

To address this, eBay will likely use escrows, badges, cross-listing, and selective Authenticity extensions to enhance trust and frictionless payments without offering full warranties. This approach will help preserve Depop’s brand while prioritizing operational improvements over insurance coverage.

Conclusion

The eBay-Allstate case reveals a key insight: insurance can greatly accelerate circular platforms, but it is selective. It works well where there are structured data, professional sellers, and high-value products, creating an environment that insurers can confidently price. These conditions are typically found in the B2B/buyer quadrant and for products like refurbished electronics. In other areas, coverage is limited: sellers must insure themselves, while peer-to-peer platforms have higher risks and thinner margins, making warranties too expensive. This creates a two-speed circular economy, where B2B platforms thrive, but peer-to-peer platforms face riskier conditions, often relying on escrows and badges instead of robust insurance coverage to manage recommerce risk.

Sources