Virtual Events, Digital Capital and Superstar Firms

A five-point checklist for platform professionals

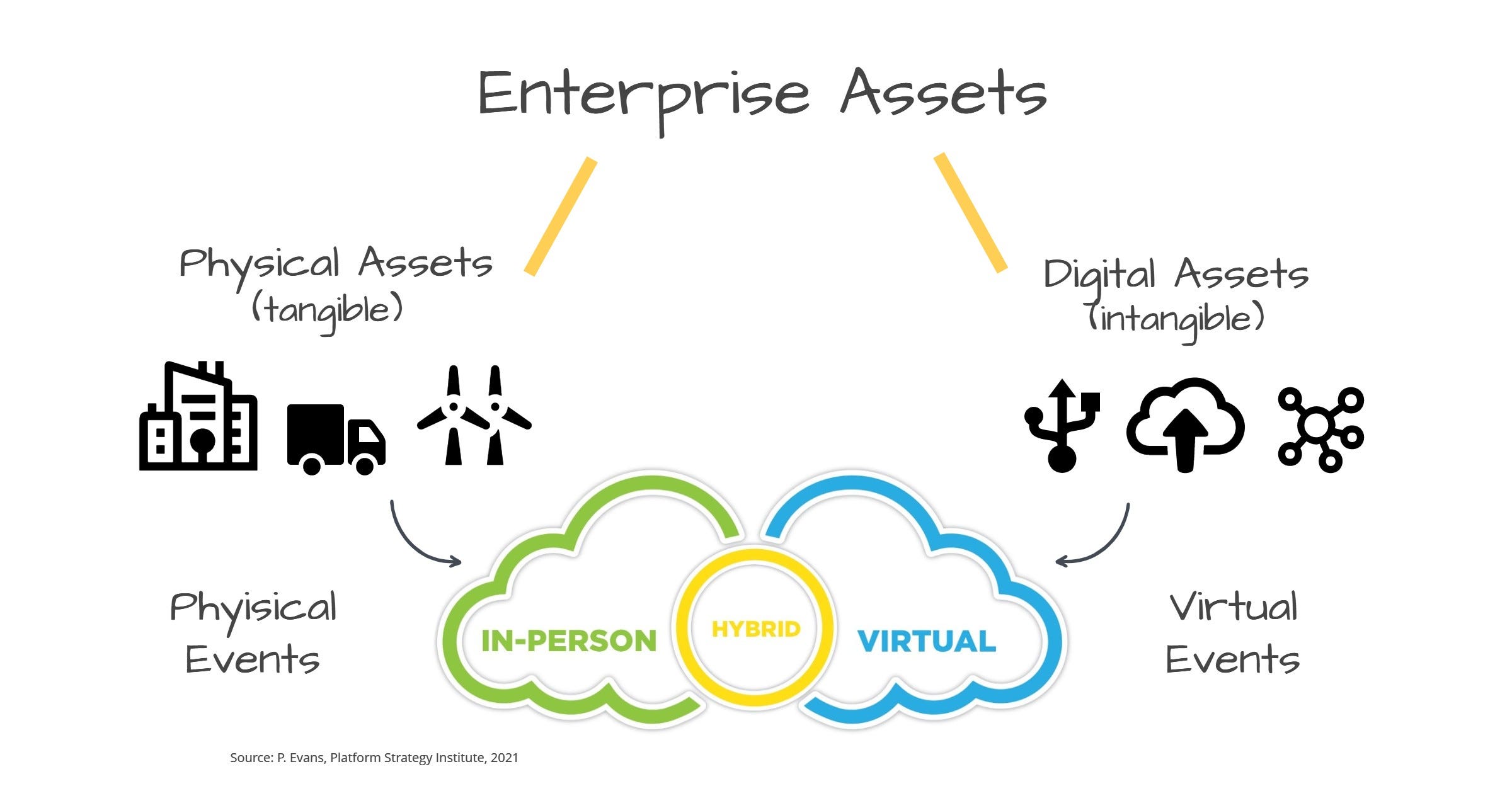

Enterprises create value by making different types of capital investments. In the past, enterprises generated significant value by investing in physical capital. Today, the tables have tilted significantly toward digital investment. Economists now find that the value of digital capital is a growing share of the economy, which has coincided with a wave of innovations based on mobile technologies, cloud computing, big data, data science, and most recently, artificial intelligence. A new paper, Digital Capital and Superstar Firms (Brookings Institution, March 2021), highlights a growing concentration of digital capital among a set of superstar firms (read platform companies), which have captured a growing share of stock market capitalization.1

Thanks to Covid, virtual events have entered the mix of digital capital investment. Most companies had some level of virtual event capability prior to last year, but it was of marginal significance for workflow, collaboration, and customer engagement. With the lockdowns and travel restrictions, this all changed dramatically. Virtual events became an essential part of doing business. Daily virtual meetings participants quickly climbed into the hundreds of millions.2

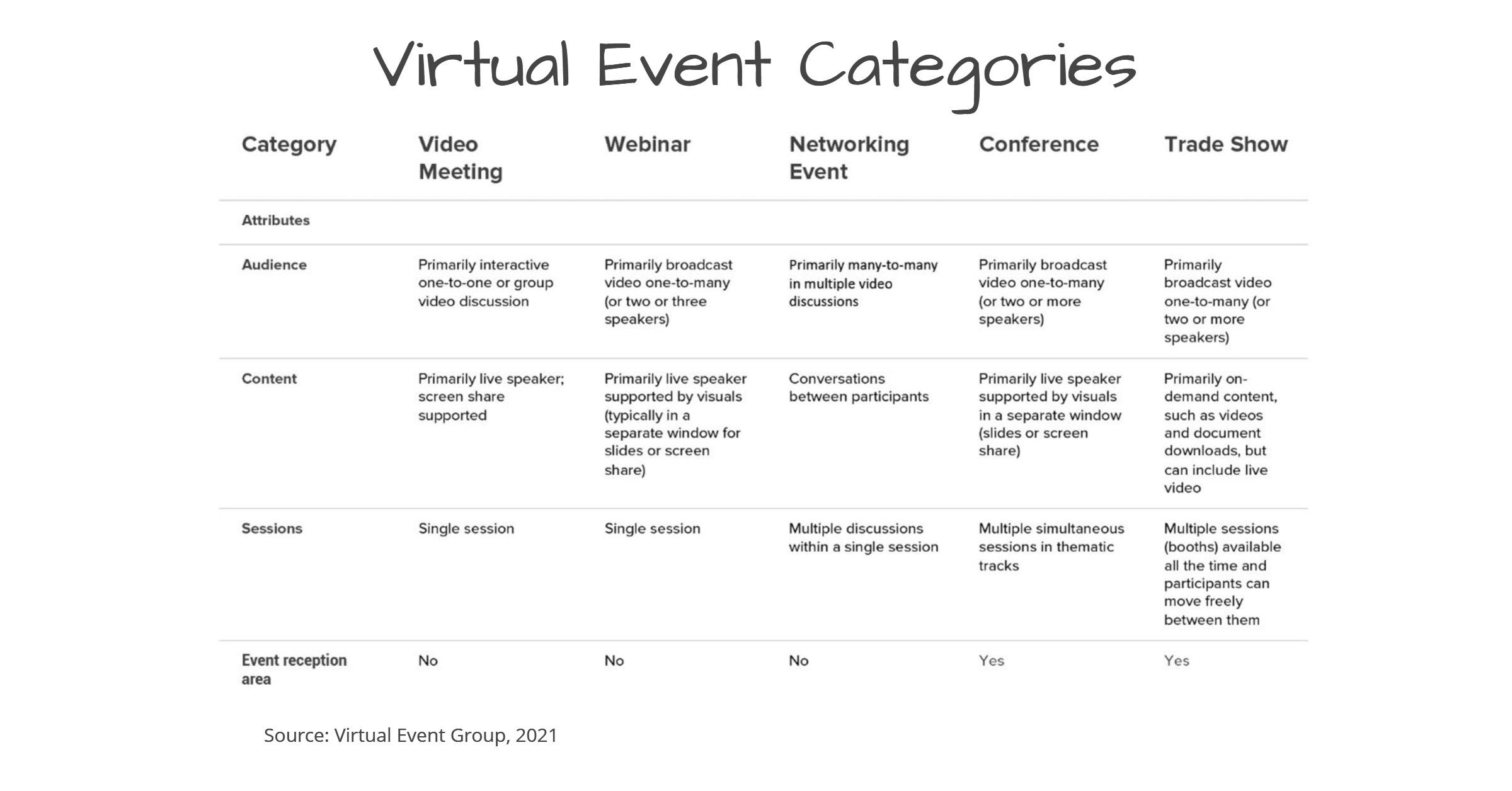

There are many types of virtual events. A useful typology has been developed by the Virtual Events Group. The table below shows five main types of events — video meetings, webinars, networking events, conferences, and trade shows— and how they can vary by audience, content, and number of sessions.

Virtual events introduce new strategic questions, which few companies have fully figured out. It is possible to leave these issues to the Events and IT teams. In many cases, these teams have done an impressive job of pivoting on a dime to the online world. However, it is doubtful that companies have maximized the full opportunity to support scale, productivity and positive network effects from virtual events.

Important insights can be gained from turning to lessons learned from platform professionals who understand platform logic, orchestration, and governance. A platform perspective can be helpful in linking virtual events to the larger project of building enterprise digital capital.

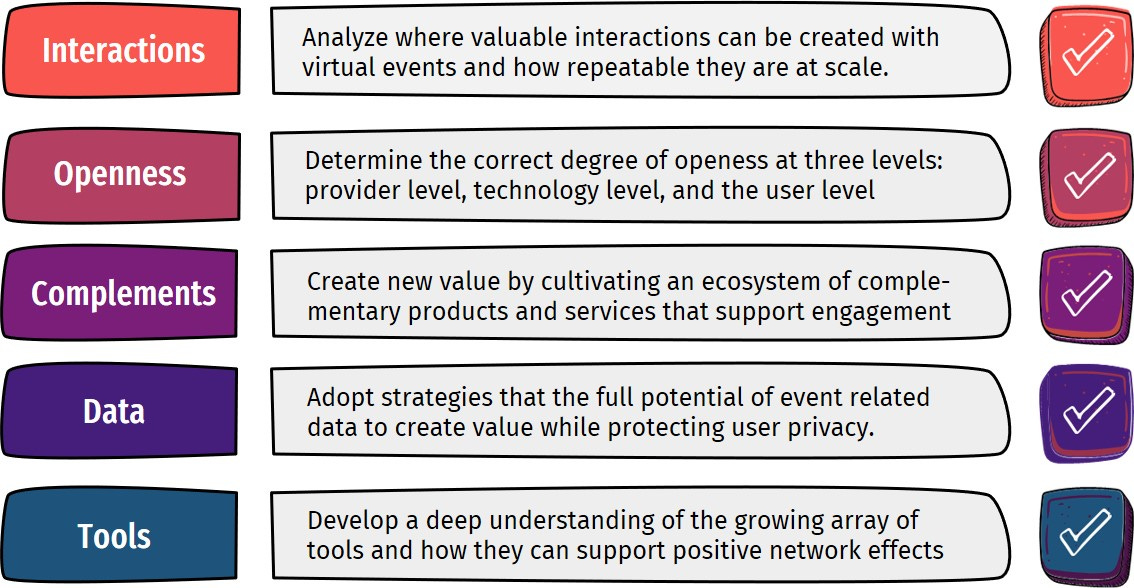

The checklist below highlights five core areas to start.

✅ Interactions

Analyze where valuable interactions can be created with virtual events and how repeatable they are at scale. One example is the Toy Association, which had been holding one major and a several regional events each year. With the shift to virtual events it found that more value could be created for members by increasing the frequency of the interactions it hosts. The Association now features Toy Fair Everywhere, a global B2B digital social marketplace, which lets both sellers and buyers grow and manage their wholesale business every day, everywhere.

✅ Openness

Determine the appropriate degree of openness for events. This will be less an issue for video meetings and webinars. However, for the larger networking, conferences, and trade shows this can be a very important source of value creation. Consideration should be given to openness at the provider level, technology level and the user level. For more on the strategic value of openness for platforms see the work of scholars like Kevin Boudreu, “Open Platform Strategies and Innovation,” Management Science, 2010.

✅ Complements

Evaluate the value that can be created by having third parties contribute to events. Careful consideration should go into determining which complements add value and on what terms. These can be complements that contribute to the core program, but they can also be centered around community and entertainment. One fun event complement I helped to provide involved securing music for the breaks at the 2020 MIT Platform Strategy Summit. With the help of the platform SideDoor, we secured the Steven Page and Craig King. Both well-known musicians broadcasted from their home studios. They were a hit with the conference participants. Check out the 10 minute video here.

✅ Data

Going virtual adds many new ways for data-driven value creation. For example, data can contribute to richer attendee engagement via more personalized, and convenient experiences. Data can also be pooled in ways that enhance discovery, match-making and other benefits that can be realized at significant scale. It is now possible to find specialized Experience Relationship Management (ERM) systems that capture, organize and analyze data associated with virtual events. For example, AnyRoad provides an ERM and sociated data intelligence tools for companies to create brand loyalty, change consumer behavior, and track metrics from virtual events.

✅ Tools

The number of tools that are available to support virtual events is growing rapidly. Large virtual event platforms like Zoom have added marketplaces with a wide array of supporting tools. The Zoom Marketplace now hosts over 200 apps that can integrate with Zoom and enhance virtual event experiences. The marketplace also includes enterprise integrations. A Salesforce integration allows users to start and schedule meetings directly within Salesforce, a feature that is also cross-marketed on the Salesforce AppExchange.

There are also a growing number of startups offering features that enhance the value of virtual events. For example, a company called Twine offers what it calls “deep networking.” Participants can join virtual breakout rooms for live 1-to-1 video convos. The length of time for the exchange can be adjusted as well as home many matches are made. Participants can engage in just one convo, or explore multiple matches back-to-back. I tried this recently and found it quite compelling. It is a great way for an event to add among participants and thereby drive cross-side network effects.

Focus on Value

Given their training and experience, platform professionals can be particularly valuable in advising how investments in virtual events can establish lasting competitive advantage. Instead of asking, “How do we make money?”, they can help to focus on the question: “How do we create and share value over the full span of interactions that virtual events afford?”

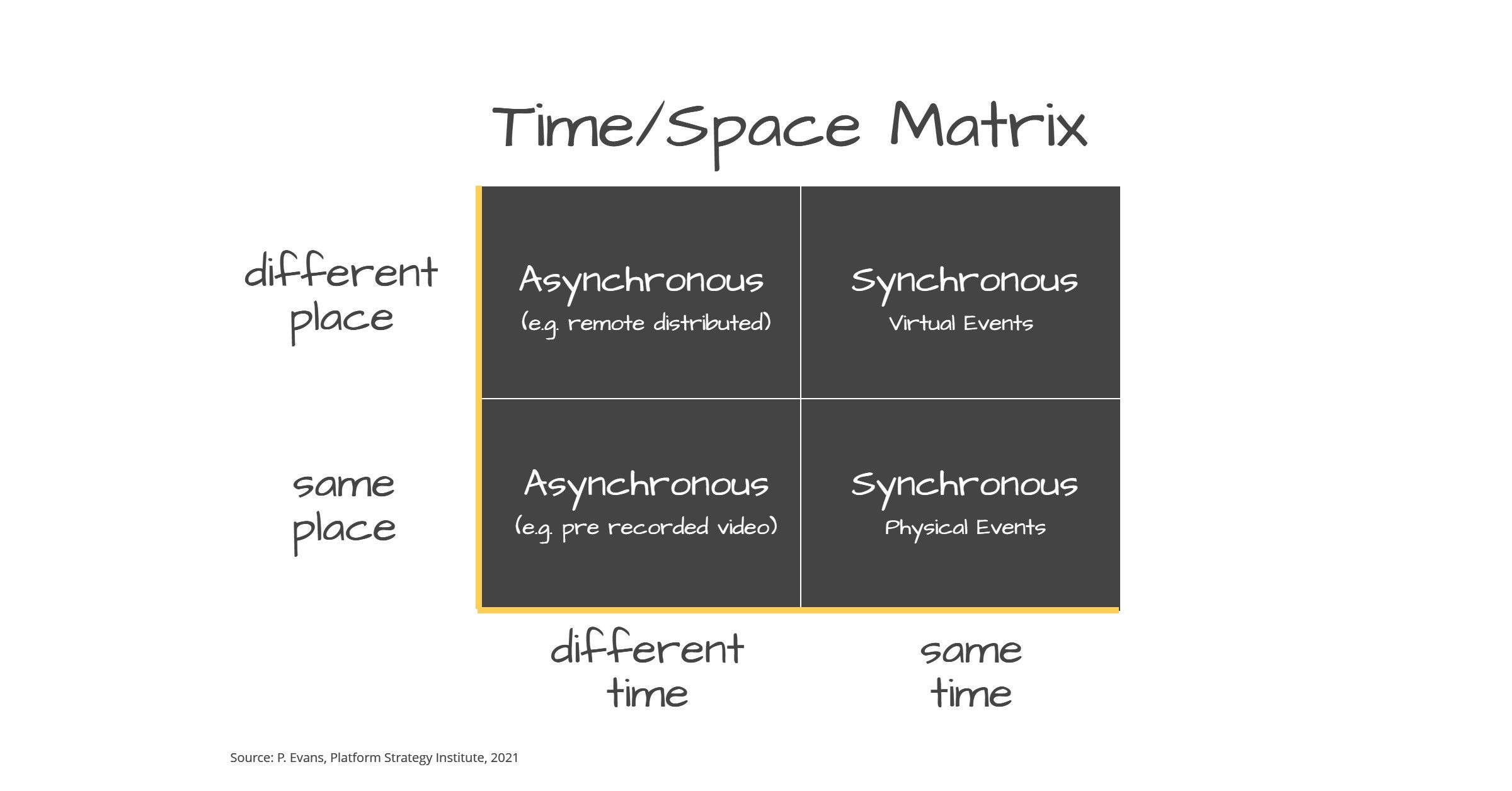

As economies reopen, companies will need to think strategically about the amount investment they make in physical verses virtual events. There is also the pros and cons of investing in real-time “synchronous” verses “asynchronous” digital opportunities, such as prerecorded content, blogs, wikis, Instagram and Ticktock posts, etc. Finally, there is the question of how these can be best tied together to secure competitive positioning and build a foundation for complementary products and services.

Although the classic time/space matrix3 aligns these to separate boxes, a platform professional will quickly realize the value created by optimizing the synergies that can be realized across the matrix. The growth of virtual experiences opens the opportunity to realize and scale both direct and indirect network effects. For example, hybrid events that combine a small physical gathering can be broadcast either synchronously or asynchronously to reach a much larger target group. As the Toy Association discovered, there can be significant advantage in increasing the frequency of interactions and thereby shift from a time in place to facilitating a community with more continuous interaction.

In short, virtual events should be considered an integral part of a company’s digital capital investment strategy. The companies that do so, and draw insights from platform design, orchestration, and governance, are more likely to land in the category of superstar firm.

Footnotes

Apple, Microsoft, Amazon and Alphabet (Google) now each have market capitalizations of over $1 trillion US dollars.

https://www.livewebinar.com/blog/50-video-conferencing-statistics-for-the-year-2020

Ellis, Clarence A., Simon J. Gibbs, and Gail Rein. "Groupware: some issues and experiences." Communications of the ACM 34, no. 1 (1991): 39-58.