Europe's Real Platform Problem

Creating platform superstar firms remains elusive

If you follow European officials and the popular press, one might think that regulation of “big tech” platforms is Europe’s main challenge. Significant attention has been focused on crafting policy measures designed to reign in platform dominance.1

In February 2020, the European Commission organized a series of events to bring together experts from European institutions and Member States to discuss the economic regulation of platforms with significant market power at European level. This culminated in the Digital Services Act package, which the European Commission submitted to the European Parliament and the European Council in December 2020. It sets forth a comprehensive set of new rules for all digital services, including social media, online market places, and other online platforms that operate in the European Union.

These proposals build on other efforts to get Europe’s digital house in order, such as the Digital Single Market package in 2016.2 Indeed, the European Commission has been aware of Europe’s weak platform position since 2015 when a staff level working group was formed to study the platform economy and frame policy responses.3

Bringing the proper oversight regarding competition policy, data privacy, and tax compliance are all important issues, no doubt. However, if we look at the most recent data on the top 100 platform firms globally, Europe has a much deeper platform challenge. Europe has been unable to create and grow large scale platforms equal to its weight in the global economy.

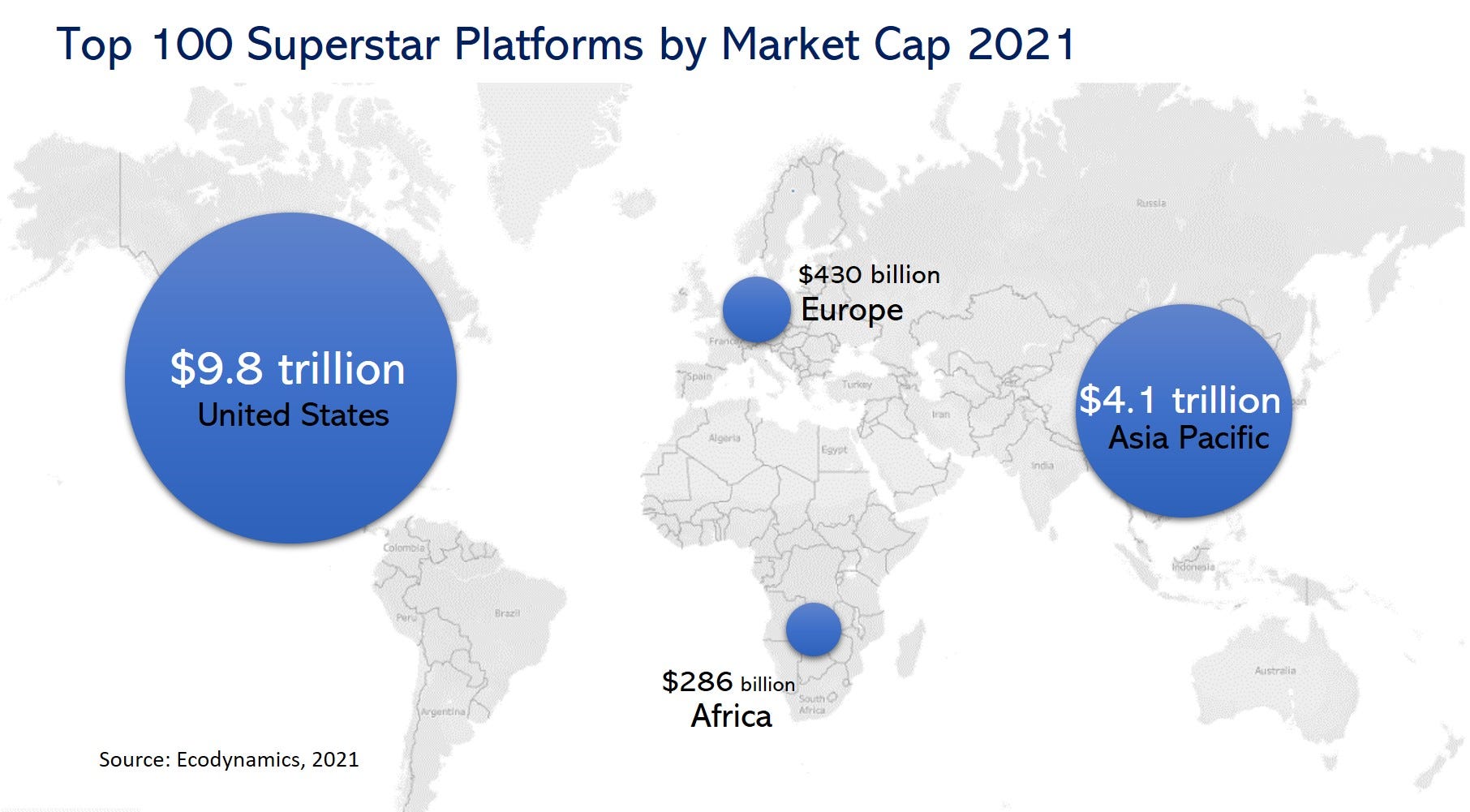

The most recent tally of the top 100 platform companies world-wide indicates shows that Europe continues to lag. According to the recent data from the Europe-based consultancy Ecodynamics, which complies a ranking of the top 100 platform firms, only 12 European platform companies make the list. This contrasts with 41 in the United States and 45 from the Asia-Pacific. More significantly, Europe only makes up 4 percent of the talent directly employed by the top 100 platforms and just 3 percent of the market valuation. The most recent results, as shown the map below, finds that Europe’s platforms have a combined market cap of $430 billion compared to $9.8 trillion for US platforms and $4.1 trillion for Asia-based platforms.

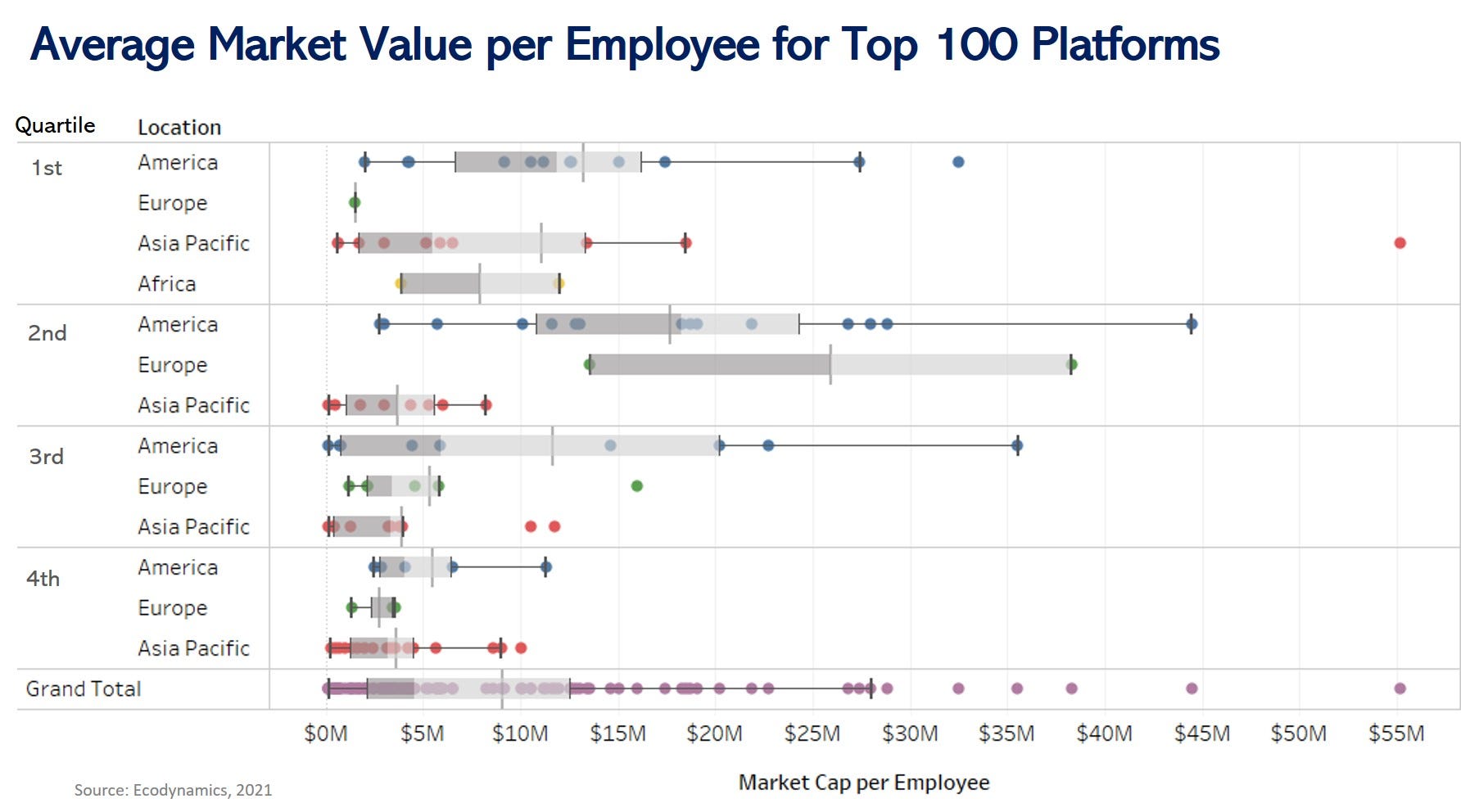

Europe also falls behind in key measures of value creation. The average market value per employee is $14 million for the 41 platform companies making the top 100 list compared to just $8M for Europe’s 12 platforms. By this measure, Europe is lagging not just in numbers and scale of the platforms but also with respect to the value created per employee.

If we look more broadly and include other regions of the world, these observations are reinforced. Europe’s largest platform perform better on average than the largest platforms in Asia but the remain behind the global average of $10 million per employee. As the figure below shows, there is some variation depending if the platform is in the top 25 companies (1st quartile), second 25 companies (2nd quartile), third 25 companies (3rd quartile) or the last 25 companies (4th quartile). Europe only registers one company in the 1st quartile and it performs well below the average of that group.

Of course, governments do not only regulate, they also engage through policies to promote innovation and economic development. This can be done through an array of tools including setting favorable standards, tax incentives, funding R&D and investing in education. These are on the table but appear to get less attention than efforts to regulate what has become known in Europe “gatekeeper” platforms.4

The private sector in Europe has also begun to focus more attention to platform strategies. For example, large industrial players, such as Siemens, ABB, BASF, VW and Shell, have launched or announced plans to launch B2B platforms. Banks and healthcare companies also have platform initiatives.5 Some have argued that The European Commission should do more to signal support for these efforts, as these companies worry, they could also be subject to horizontal and vertical competition law issues aimed at the “gatekeeper” platforms.6

There is also more attention to galvanizing a European startup scene and encourage more European-based entrepreneurship.7 There are now more European startups pursuing platform business models. Some European VCs, such as SpeedInvest, have even framed their investment thesis around European early-stage startups that harness network effects and have a chance to become category leaders.

Still, the latest tally suggests that Europe’s ability to generate platform superstar firms remains elusive.

I’m looking forward the presenting on the race for platform talent at a webinar hosted by Platform Innovation. This international webinar will take place on Feb 25th at 8AM EST, 2PM CET and 9PM SGT.

For a detailed look at the type of platform talent that companies need to position and win in the platform economy, please see:

https://voxeu.org/article/self-preferencing-gatekeeper-platforms-implications-digital-regulation

https://www.eu-startups.com/