Circular Fintech Solutions for Secondary Market Platforms

Wireless repair industry example | Credit Key + MobileSentrix

As the circular economy grows in size and scale, it is increasingly attracting the attention of fintech companies. By integrating financial services directly into circular platforms, fintechs are helping to overcome a key barrier to circularity: access to affordable, low-friction financing. This is especially crucial for small and medium-sized enterprises (SMEs), who often lack the capital or the resources to spend on financial products that have high administrative costs. Without flexible and highly automated financial products, many businesses can struggle to participate in secondary markets, limiting the flow of goods and undermining the ability to scale the circular economy.

Companies like Credit Key are now offering instant credit and embedded financing options that empower businesses to purchase circular goods and services without straining cash flow. Their integration with companies such as MobileSentrix, a leading supplier in the wireless repair industry, demonstrates how fintech is making it easier for merchants and buyers to participate in the secondary market for electronics. By providing real-time credit decisions and flexible payment terms directly within the purchasing workflow, these fintech solutions are removing barriers to entry, increasing transaction volume, and enabling more businesses to grow the circular economy. As a result, fintech is becoming a critical enabler of driving the scale.

Circular Fintech

Circular fintech refers to financial technologies, products, and services specifically designed to support and accelerate transactions within the circular economy. Platforms and services in the circular fintech sector are designed to allocate capital to projects and companies that prioritize circularity, such as those involved in recycling, refurbishing, or sharing platforms. They help mitigate financial risks for circular businesses by offering flexible terms and tailored credit assessments, and they encourage sustainable consumption and production by making circular options more accessible and affordable.1

When companies seeking to buy and sell in secondary markets do not have access to financing, several significant consequences arise that can hinder the growth of the circular economy. Most notably, the lack of financing leads to reduced transaction volume, as many businesses—especially small and medium-sized enterprises—simply cannot afford to purchase inventory or invest in circular assets without external financial support. This limitation in liquidity affects both buyers and sellers: sellers may struggle to find buyers able to pay upfront, while buyers often miss out on opportunities to acquire valuable secondary goods or materials. As a result, fewer transactions take place, directly undermining the core principle of the circular economy, which depends on the continuous reuse and recycling of products and materials.2

Additionally, companies that lack access to affordable financing may face higher borrowing costs or be forced to accept less favorable terms, making circular business models less competitive compared to traditional linear models that typically enjoy better access to finance. This financial disadvantage slows the growth and innovation of circular businesses, as they are less able to scale their operations, invest in new technologies, or expand into new markets. The absence of accessible financing also creates barriers to entry for new or smaller players, who often lack the collateral or credit history needed to secure loans or credit lines, effectively excluding them from participating in secondary markets.

Circular fintech solutions can help overcoming these barriers. This includes facilitating access to capital for circular business models as well as providing the digital infrastructure, tools, and automation needed to enable low-friction transactions. Circular fintech also leverages digital tools such as blockchain, IoT, and artificial intelligence to promote transparency and traceability, ensuring accountability and sustainability in financial and material flows.

Automotive Sector

Circular fintech solutions are well established in the automotive sector. Cox Automotive provides financing solutions for car dealers to purchase and hold used car inventory through its subsidiary, NextGear Capital. NextGear Capital is a leading provider of floor plan lending products and services, offering flexible lines of credit that allow dealers to finance nearly any type of remarketed unit—including retail, wholesale, salvage, and rental vehicles.3

These floor plan lines of credit function much like a credit card for inventory: dealers can use their credit line to acquire vehicles from over 1,000 live and online auctions, as well as through dealer-to-dealer purchases, trade-ins, and off-street sources. Dealers pay interest on the amount borrowed until each vehicle is sold, and as inventory sells, the original loan is repaid. NextGear Capital’s solutions are customizable, with competitive rates, flexible terms, and digital management tools for funding, title tracking, and more.

Cox Automotive’s NextGear Capital also offers enhancements such as the Flex Pricing program, which provides principal reductions and payment deferments, helping independent dealers manage cash flow and inventory costs more effectively. The platform is designed to help dealers expand their inventory, improve cash flow, and streamline the process of acquiring and remarketing used vehicles.

Circular Finance for Electronics

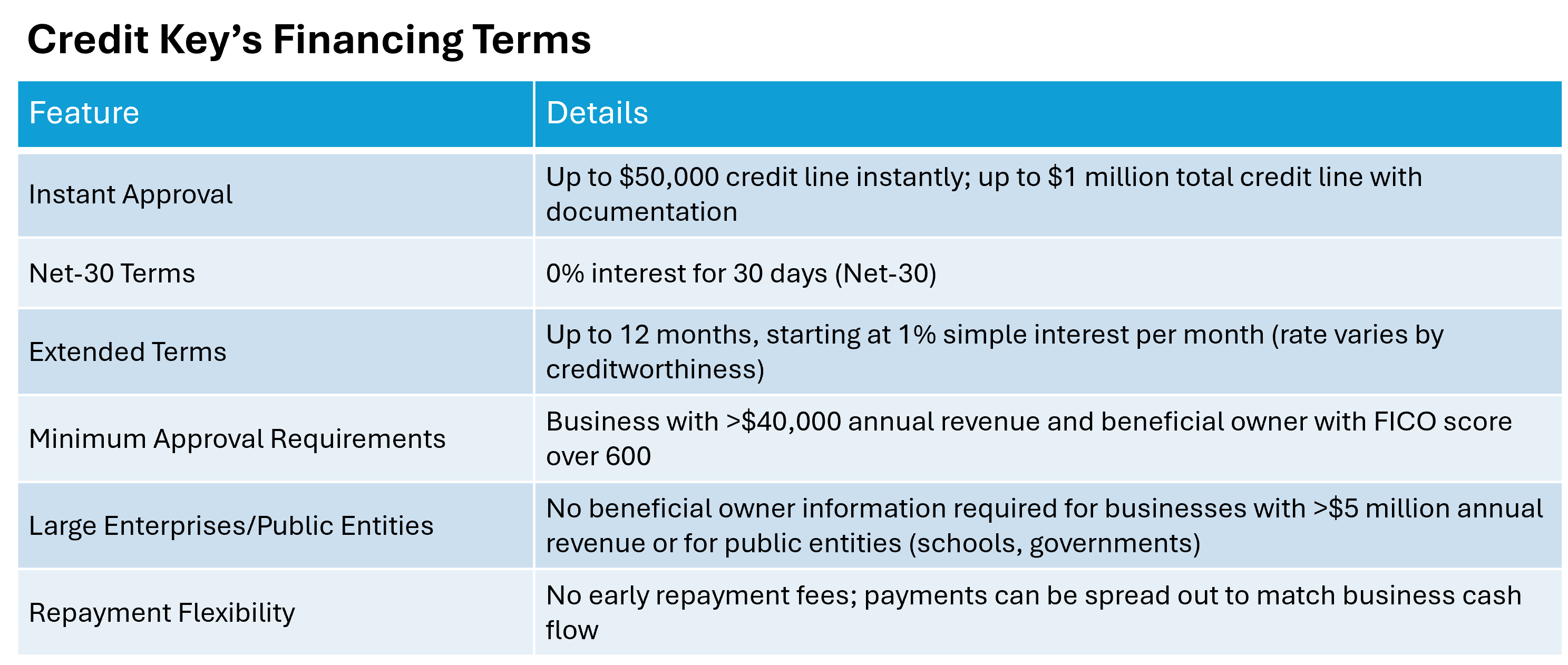

Credit Key is an example of circular fintech solutions developed for the electronics sector. This fintech company provides short-term, flexible financing for business-to-business transactions. With Credit Key, companies can purchase essential goods and services, including circular or sustainable products, without straining their cash flow. The company offers instant approvals for credit lines up to $50,000, which can be extended to $1 million with additional documentation. All approved customers receive Net-30 terms, meaning 0% interest for the first 30 days, and extended terms are available for up to 12 months, starting at 1% simple interest per month, with rates varying based on business creditworthiness. To be approved, a business must have more than $40,000 in annual revenue and a beneficial owner with a FICO score over 600. For larger enterprises with over $5 million in annual revenue and public entities like schools and governments, beneficial owner information is not required to apply. Repayment is flexible, with no early repayment fees, allowing businesses to align payments with their cash flow.

Credit Key offers short-term B2B financing through a partnership with Lead Bank, which originates certain business-purpose loans provided via the Credit Key platform. Credit Key itself is not a bank; it facilitates instant credit decisions and flexible payment terms for business buyers, while Lead Bank underwrites and issues the loans subject to credit approval. This partnership enables Credit Key to provide seamless, embedded financing solutions for B2B transactions across various eCommerce and ERP platforms.

Credit Key leverages APIs and pre-built integrations to embed flexible financing solutions into top B2B eCommerce platforms like BigCommerce, NetSuite, Magento, Shopify, and WooCommerce. By integrating Credit Key's API or platform extensions directly into the merchant's checkout and sales workflows.4 This API-driven integration enables real-time underwriting powered by AI, allowing buyers to apply for and receive instant credit lines (up to $50,000 or more) right at checkout, whether online, in-store, or through sales representatives. Merchants get paid upfront—often within 48 hours—while Credit Key assumes the credit risk and handles collections, eliminating the administrative burden and financial uncertainty usually associated with extending net terms.

By embedding financing directly into online platforms, Credit Key increases customers' purchasing power and payment flexibility, driving higher average order values (AOV) and reducing cart abandonment. This improved purchasing experience encourages buyers to spend more and more frequently, thereby increasing gross merchandise value (GMV) for merchants. The integration also supports omnichannel sales, enabling financing offers across online stores, physical points of sale, and offline sales teams, which amplifies network effects as more buyers and sellers engage with the platform.

The range of financing options and approval rates offered by each platform also matters. Platforms with broader lender networks are likely to provide higher approval rates and more tailored financing for diverse customer segments, directly influencing customer satisfaction and repeat business. Additionally, embedded lending solutions can generate valuable data insights into customer behavior and financing trends, enabling merchants to refine their marketing and inventory strategies. Some platforms also allow merchants to share in loan origination or financing fees, offering a new revenue stream beyond core retail sales.

For lenders, integrating with platforms opens up access to a larger and often pre-qualified customer base, increasing loan origination volume and reducing customer acquisition costs. Access to transaction and behavioral data from retail partners also allows lenders to perform more accurate credit assessments, potentially reducing default rates and improving portfolio performance. Operational efficiency is another benefit, as digital integration and automation streamline loan origination, underwriting, and servicing processes, reducing manual workloads and enabling lenders to adapt quickly to changing market demands.

Wireless repair industry example

Repair services play a crucial role in improving resource loops by allowing devices and their components to be used, refurbished, and eventually recycled. MobileSentrix, a prominent wholesale supplier in the wireless repair industry, specializes in distributing cell phone repair parts and related products.5 Founded in 2014 and headquartered in Manassas, Virginia, the company has grown to become one of the major players in the sector, serving the growing number of domestic and international repair shops. MobileSentrix offers a comprehensive range of cell phone parts for major brands like Apple, Samsung, Motorola, and Google, as well as proprietary product lines, including Casper premium tempered glass, XO5 True Tone screens, AmpSentrix certified batteries, and ScrewBox iPhone screw kits.

The company's SWAP Program lets repair shops send in cracked screens and receive ready-to-install replacements. They also offer professionally graded, GSM unlocked, and guaranteed crack-free pre-owned devices with excellent battery health, such as iPhones, iPads, Galaxy, Motorola, and Pixel models. In addition to parts and devices, Mobile Sentrix supplies accessories like high-speed cables, chargers, and specialized repair tools.

As a business-to-business wholesaler, MobileSentrix requires business documentation for account approval. They're known for offering lifetime warranties on parts (excluding accidental damage or misuse), a buyback program for broken LCDs, and a suite of online integration tools for inventory management and direct drop-shipping. The company is recognized for its aggressive pricing, exceptional customer service, and fast delivery, with most orders processed and shipped within 24 hours. They also accept cryptocurrency payments and provide Amazon Shipping as a fulfillment option.

Credit Key's circular financing enables MobileSentrix's business customers to access flexible payment options directly at the point of purchase. When shopping with Mobile Sentrix, customers can apply for instant business credit through Credit Key, receiving a real-time decision for a line of credit up to $50,000—or sometimes even higher with additional information. They can then choose from various payment terms, including Net 30, four interest-free installments, or extended repayment plans up to 12 months.

This approach lets MobileSentrix's customers buy now and pay over time, making larger purchases more manageable and improving their cash flow. Meanwhile, MobileSentrix receives full payment for the order within 48 hours, as Credit Key assumes 100% of the payment risk and handles all collections. This eliminates the need for MobileSentrix to manage in-house trade credit or chase down payments, streamlining their operations and boosting sales by removing barriers for customers who might otherwise be limited by cash flow or traditional financing options. Credit Key's integration with e-commerce and order management systems ensures a low-friction experience for both MobileSentrix and its customers, enhancing conversion rates and customer loyalty by offering a convenient, frictionless financing solution tailored to the needs of modern B2B buyers.6

Conclusion

Circular fintech helps businesses invest in circular products and services, such as refurbished equipment or recycled materials, without the burden of significant upfront costs. This reduces barriers for small and medium-sized enterprises to participate in the circular economy and enables scale. Looking ahead, we can expect to see even more embedded financing options across a wider range of recommerce platforms, making it easier for businesses and consumers alike to participate in the circular economy. Platforms will be able to offer a variety of financing products directly at the point of sale. Overall, circular fintech solutions will play a critical role in scaling circular platforms by increasing transaction speed, improving trust, and making higher-value secondary purchases accessible to more businesses and consumers.

References

Grégoire, Vincent, and Kevin Guay. "Circular Economy: A Fintech Driven Solution for Sustainable Practices." In Fintech and Sustainability: How Financial Technologies Can Help Address Today’s Environmental and Societal Challenges, pp. 149-168. Cham: Springer Nature Switzerland, 2023.

Takacs, Fabian, Dunia Brunner, and Karolin Frankenberger. "Barriers to a circular economy in small-and medium-sized enterprises and their integration in a sustainable strategic management framework." Journal of Cleaner Production 362 (2022): 132227.