From War Damage to Rapid Reconstruction

How Digital Recommerce Platforms Can Overcome OEM Bottlenecks on Oil & Gas Equipment

Introduction

The war with Iran that started on February 28, 2026, has severely damaged Middle East oil and gas infrastructure. Early estimates put the total infrastructure damage at up to $58 billion. This estimate includes damage to over 80 oil and gas facilities, and the costs could rise if the war continues. At the same time, rebuilding efforts face two major challenges: the financial cost and long lead times for new equipment, which can take from 9 months to 5 years due to supply chain issues and high global demand for the same types of equipment outside the Middle East.

The current situation highlights the need for the oil and gas industry to use digital recommerce platforms to their full potential. These platforms, which specialize in finding and selling surplus and reconditioned equipment, can access large amounts of surplus and used equipment from around the world. This equipment can be delivered faster and at a lower cost. This article examines the extent of the damage, quantifies the delays, and identifies large amounts of idle oil and gas equipment. It also outlines three ways for oil companies to source equipment, addresses key obstacles, and features platforms like IronHub, which can bring significant benefits in speed, cost, and resilience, building on its successful use in Canada to achieve global impact.

Damage Estimates

The damage assessments show a severe but uneven impact on Middle East oil and gas infrastructure. Rystad Energy estimates the repair costs to be between $34 billion and $58 billion and over 80 facilities affected, some severely.1 The most damage is in Qatar, Iran, the UAE, Saudi Arabia, and Kuwait, with Qatar’s Ras Laffan LNG complex being one of the most disruptive cases.

Various facilities were damaged or disrupted, including refineries, gas-processing plants, LNG trains, pipelines, production fields, export terminals, and ports. Notable incidents include damage to Qatar’s Ras Laffan LNG site, Iran’s South Pars gas field, Abu Dhabi’s Habshan and Das Island gas assets, and Saudi gas and refining infrastructure.

Qatar is particularly affected because the Ras Laffan attack took about 17% of global LNG supply offline, and repairs could take two to five years, resulting in around $20 billion in lost annual income.2 Iran’s infrastructure is also heavily damaged, with estimated repair costs near $19 billion. Other Gulf states experienced serious interruptions, but some were more reversible, such as temporary shutdowns or lower output due to export constraints.

The main concern is not just the repair cost, but how long it will take to recover. Several reports warn that shortages of critical equipment and skilled labor could keep some assets offline for years.3 This means the conflict will likely limit regional oil and gas output long after the fighting stops, especially for LNG and other export-dependent infrastructure.

Lead times

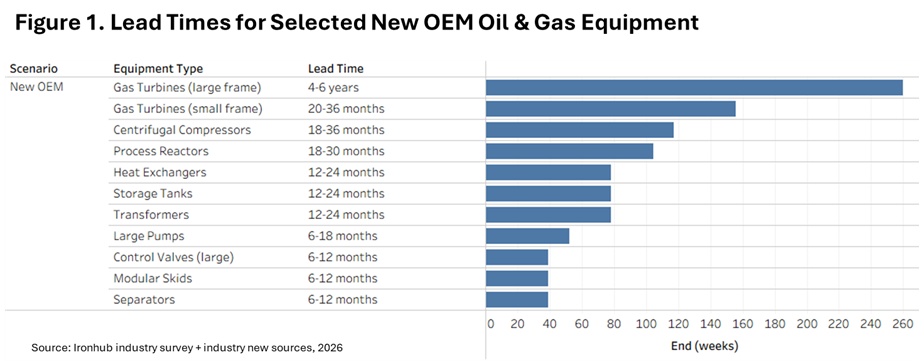

A major challenge in reconstruction is the long lead times for new OEM equipment. Table 1 shows the delays in weeks for different categories. Large frame gas turbines have the longest lead time at 260 weeks, which is roughly 5 years. Small frame gas turbines take around 156 weeks, or about 3 years. Centrifugal compressors have a lead time of 117.3 weeks, which is over 2 years. Process reactors take 104.3 weeks, while heat exchangers, storage tanks, and transformers each take 78.2 weeks, or around 18 months. Large pumps require 52.1 weeks, and control valves, modular skids, and separators take about 39.2 weeks each, or around 9 months.

The long lead times for new OEM oil and gas equipment are due to global supply chain bottlenecks, sudden increases in demand, and limited manufacturing capacity among specialized suppliers.4 Reconstruction efforts in the Middle East and growing demand for data centers and power worldwide have filled up order books, especially for complex items like large frame gas turbines and compressors. Utilities and developers are competing fiercely, with some OEMs booked solid through 2029-2030.

Making these components requires rare materials, precise forging, and complex supply chains that are slow to grow. Testing also takes months to prepare, and a shortage of skilled labor adds to the delays. Some critical parts, like forgings, have their own multi-year backlogs, made worse by years of underinvestment in fossil fuel equipment due to trends towards electrification and changes in regulations. Using refurbished or used equipment, which can be available in 3-6 months, is becoming an important workaround.

Alternative Equipment Sourcing Strategies

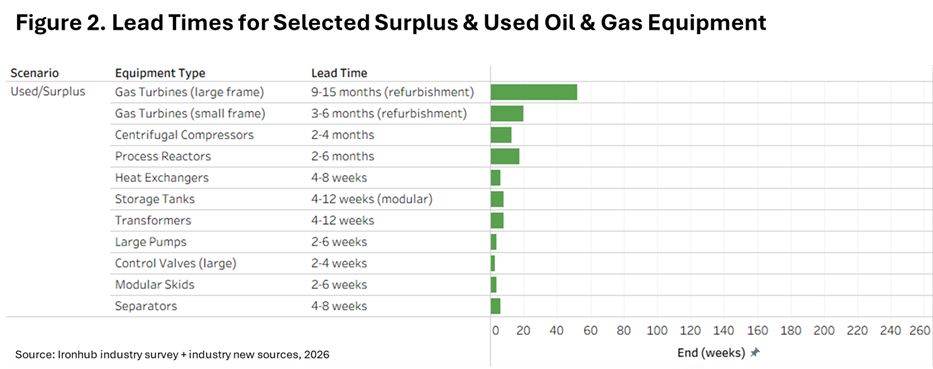

The attached “Used-Surplus-O-G-Equipment-Lead-Times.xlsx” shows that used and surplus oil & gas equipment have much shorter lead times than new OEM options. The lead times, listed in weeks, cover different refurbishment and delivery scenarios, highlighting the availability of equipment for quick deployment in reconstruction projects.

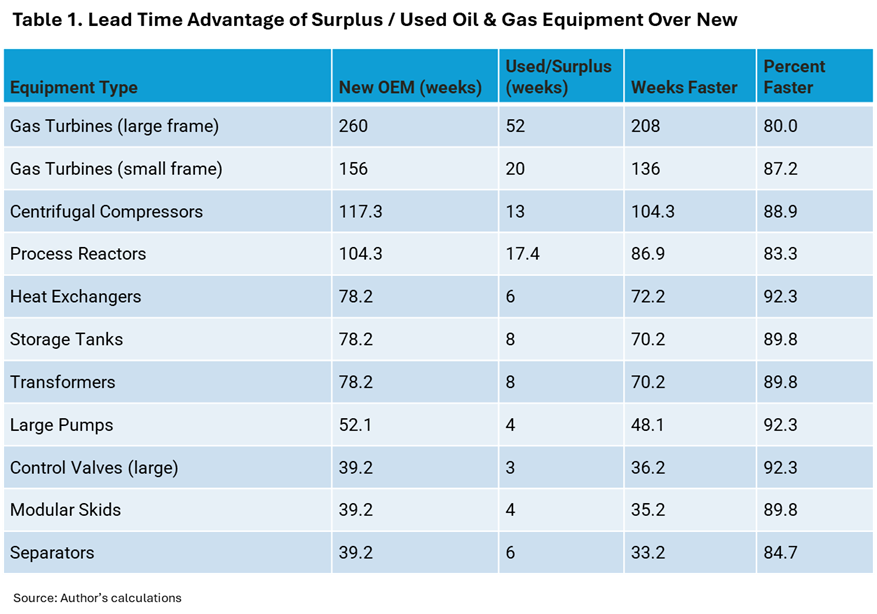

Using used or surplus oil & gas equipment can save a lot of time compared to new OEM alternatives, often reducing lead times by 84-92% across categories. This can free up several months to years for urgent reconstruction projects.

For large frame gas turbines, used or surplus options can cut delivery times from 260 weeks (5 years) to 52 weeks, which is 208 weeks (48 months) faster, or 80% quicker. This enables projects delayed by OEM backlogs to restart within a year. Small frame gas turbines see an even bigger improvement, with delivery times dropping from 156 weeks to 20 weeks, saving 136 weeks (31 months) or 87% of the time. As a result, operational power generation can start in under 6 months instead of taking 3 years.

Simpler gear also shows similar advantages: centrifugal compressors can be delivered in 13 weeks, down from 117 weeks, which is a 104-week reduction, or 89% faster. Heat exchangers are reduced from 78 weeks to 6 weeks, saving 72 weeks, or a 92% reduction, allowing for rapid integration into processing trains. These examples show how surplus markets can speed up rebuilds by years for important items, avoiding the global supply crunch for new equipment.

On average, used or surplus options are 84-92% faster across categories, saving 7.7 to 48 months, which is critical for urgent reconstruction when new OEM delays can take up to 5 years. Gas turbines see the biggest time savings, up to 208 weeks faster, while simpler items like valves and pumps can be deployed almost immediately. This makes surplus markets a key way to accelerate progress during supply crises.

Used and surplus oil & gas equipment usually costs 30-70% less than new OEM prices, depending on its condition, age, how much it’s been refurbished, and what buyers are willing to pay.

Surplus gear sold “as-is” from auctions, liquidations, or overstock can be 50-70% cheaper than new equipment, making it a good option for applications that don’t need high specs, but it comes with more risk. Reconditioned or refurbished units, which often have warranties, typically cost 30-60% less than new ones, offering a balance between cost and reliability - for example, rebuilt tanks or pumps can cost half as much as new ones. OEM-certified pre-owned equipment might only be 20-40% cheaper, but it includes full support and less risk of downtime.

Buyers benefit from avoiding long wait times and can source equipment flexibly through auctions or brokers, which helps minimize storage costs.5 For instance, a new small frame gas turbine costing $22-35 million might be available used or refurbished for $9-16 million, a 30-60% discount that allows for faster and cheaper reconstruction. It’s essential to consider inspection and transport costs, which can add 5-15%, but still result in overall savings.

How Much Surplus and Used Equipment is Available?

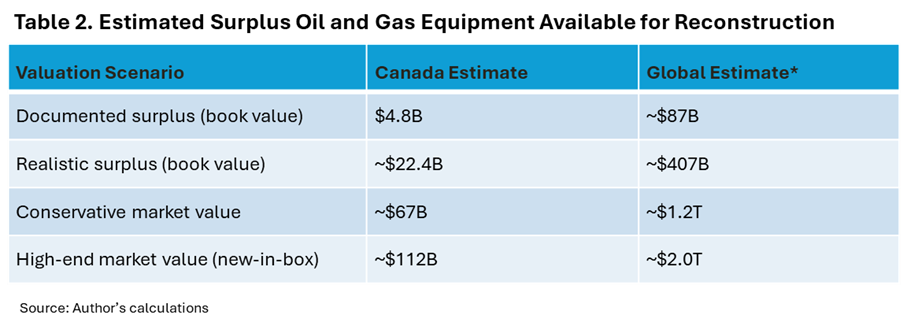

To determine the amount of oil and gas equipment available for reconstruction efforts, IronHub analyzed the Canadian upstream sector. The analysis examined the top 30 producers in Canada, excluding the two largest integrated producers, and found that approximately 3% of their total Property, Plant, and Equipment (PP&E) book value was listed as surplus. This surplus is worth around $4.8 billion. However, this figure only captures the surplus that operators have officially recognized. When including undocumented surplus, the estimate increases to approximately 7% of PP&E. When the two largest integrated producers are included, the total Canadian surplus reaches approximately $22.4 billion at this higher estimate.

Canada produces about 5.5% of the world’s upstream oil and gas. Applying the same methodology globally reveals the scale of idle equipment worldwide. If 3% to 7% of the estimated $4 to $5 trillion in global upstream PP&E is surplus, then the known surplus equipment is worth $120 billion to $150 billion. A more realistic estimate is $280 billion to $350 billion. Even at the most conservative level, this means over $100 billion in surplus equipment is available. The central problem for reconstruction in the Middle East is not a shortage of equipment — it is the difficulty of finding and accessing it.

It is also important to distinguish between book value and market value. The oil and gas industry usually uses aggressive depreciation schedules, around 25% per year, which can reduce the book value of equipment to almost zero. However, a significant portion of this equipment is new, unused, and still in its original packaging, with market values much higher than their depreciated book values. Using conservative fair market value estimates, IronHub calculates that surplus equipment in Canada is worth over $50 billion. On a global scale, idle inventory held by operators could be worth hundreds of billions, possibly over a trillion dollars, in equipment that could support reconstruction without needing new production.

The amount of surplus oil and gas equipment available for reconstruction is substantial, even with conservative estimates, and much larger when considering market values. At book value, the estimated surplus in Canada ranges from $4.8 billion to $22.4 billion, while globally it ranges from $87 billion to $407 billion. When using fair market value, the opportunity becomes much larger: the same equipment could be worth $67 billion to $112 billion in Canada and up to $1.2 trillion to $2.0 trillion globally. This means the problem is not having enough equipment, but rather finding, accessing, and redeploying it quickly to meet reconstruction needs.

The size of this idle inventory changes how we look at the reconstruction challenge: instead of wondering if there’s enough equipment to rebuild oil and gas infrastructure in the Middle East, we should be asking if operators have the right tools and processes to find and use it. The tools and processes needed are discussed below.

How IOCs, NOCs, and EPCs can use secondary platforms to secure equipment

Operators and their contractors, including IOCs, NOCs, and EPCs, can use secondary platforms and markets to get used and surplus equipment for quick reconstruction. This way, they can avoid the long wait times of up to 5 years for new equipment from the original manufacturers. There are three main ways to do this, each with its own advantages in terms of speed and cost, offering discounts of 30-70%. Let’s look at each one and the practical steps to take to use digital platforms to speed up access.

Pathway 1: Internal Sourcing—Using Your Own Assets

The easiest and fastest way is to look at what you already have. Many large NOCs and IOCs have the equipment they need, but it’s just sitting idle in yards, warehouses, or fields that are not being used. For example, a compressor might be sitting in a yard in Kuwait while a team in Dubai is ordering a new one. Platforms like asset management systems, such as SAP EAM or Oracle, or internal marketplaces, like GE’s asset hubs, can look at all your assets in real-time and match what you have to what you need in just a few days, instead of months. For instance, Aramco or ADNOC could move separators from storage in their own country, which would take 6 weeks, and save 33 weeks compared to waiting for new equipment, which would take 39.2 weeks.

Pathway 2: Peer-to-Peer Sharing—Using Each Other’s Surplus

One operator’s extra equipment can be just what another operator needs. Secondary platforms like Oilpatch Surplus, Surplus Energy Equipment, or new marketplaces that use blockchain allow operators to find what they need from each other. For example, QatarEnergy could list heat exchangers that are not being used, which could be delivered in 6 weeks, and Petronas, which needs them quickly, could buy them instead of waiting 78 weeks for new ones. A small gas turbine that is not being used could be moved from TotalEnergies’ yard to an EPC that is rebuilding facilities in the UAE, saving 136 weeks.

Pathway 3: EPC and Third-Party Sourcing—Unlock Global Inventory

EPCs often default to OEMs due to vendor lists and liability concerns, but platforms like IronPlanet, Salvex, and High Country Sales bring together global surplus inventory from auctions, liquidations, and brokers. This offers faster access to equipment, such as control valves, which can be delivered in 3 weeks compared to 39 weeks for new ones. Companies like Bechtel and Fluor can integrate this inventory into their RFQs through API feeds, ensuring “plug-and-play” gear, like modular skids, which can be delivered in 4 weeks when used. For large-scale projects in the Middle East, like Ras Laffan rebuilds, this sourcing method can provide transformers in 8 weeks, cutting 70 weeks off the typical delivery time for new equipment.

By using these platforms, the average sourcing time can be reduced from 104 weeks to under 20, which can significantly change the economics of reconstruction, especially when combined with 50-70% cost savings on high-value items like turbines. IOCs and NOCs should consider piloting cross-pathway dashboards for their 2026 projects now.

There are three main challenges to securing used and surplus oil and gas equipment for reconstruction: limited visibility, lack of data standardization, and barriers to EPC adoption. These issues, which affect all three pathways, prevent the industry from achieving the 84-92% faster timelines and 30-70% cost savings that secondary markets can offer.

Visibility Gaps

Operators do not have real-time views of surplus assets, whether they are internal or held by peers. These assets are often hidden in separate spreadsheets, old ERPs, or unlogged storage areas - for example, a compressor might sit idle in Basra while Kuwait orders a new one. There is no clear owner of surplus asset redeployment, and procurement metrics focus on new purchases rather than inventory checks, making internal sourcing rare even though it can save time.

Data Standardization Deficits

Incomplete and inconsistent data prevent transactions from happening across the industry. For instance, what Aramco calls a “high-pressure separator vessel” might be referred to as a “production separator - HP stage” by Petrobras, with no standard specifications for things like manufacturer, model, condition, and material grades. Without a digital record of product details or a common language, buyers cannot properly evaluate offers, which slows down peer-to-peer sales.

EPC Adoption Barriers

EPCs tend to stick with original equipment manufacturers because there is no single, reliable source of global inventory information. Details like ASME ratings, service history, and inspection records are often missing, and concerns about liability and matching specifications make companies rely on approved vendor lists. Even readily available surplus items, like control valves that can be installed in three weeks, are overlooked in favor of new ones that take 39 weeks to deliver.

All of these issues share a common problem: the platforms for finding and buying surplus assets are not well-developed, and there is a cultural preference for new equipment. The incentives for procurement are also misaligned, prioritizing the purchase of new items over efficient reuse, which means that significant time and cost savings are being missed until the data and processes improve.

Regional Platforms: Lessons from Canada

The barriers mentioned earlier—visibility gaps, data fragmentation, and EPC reluctance—are real, but they can be overcome. Canada’s oil and gas sector provides a useful example of what happens when a regional market commits to digitizing surplus inventory on a large scale.

In recent years, independent recommerce platforms in the Canadian upstream sector have shown that it is possible to aggregate, standardize, and verify surplus equipment across multiple operators. This is done by bringing producers onto a shared platform where idle assets are cataloged in detail, including photos, pressure ratings, material grades, service history, and condition assessments. The result is a searchable, trusted inventory that sits above what were previously disconnected spreadsheets and unlogged yards.6

The Canadian experience is revealing for several reasons. First, it shows that operators are willing to participate when the platform offers a clear financial benefit, rather than just asking them to contribute data. When producers can recover significant capital from idle assets, the business case for participation becomes clear.

Second, the Canadian market has shown that standardization is a problem that can be solved at the regional level. By using a common taxonomy, different operators’ descriptions of the same equipment can be reconciled, making it easier for buyers and sellers to find what they need. This is especially important for EPCs, whose engineers need to evaluate equipment against specific technical specifications.

Third, and perhaps most importantly for Middle East reconstruction, the Canadian model has proven that redeployment timelines can be much shorter than buying new equipment. In practice, equipment that would have sat idle has been moved to active projects within weeks of being listed.

However, the limitations of the Canadian precedent should be acknowledged. Canada’s upstream sector is relatively small, with a manageable number of large producers operating under consistent regulations and in close proximity. Replicating this model in the Middle East, with its fragmented and geographically dispersed landscape, is a much harder problem.

Still, the key insight remains: the main constraint on rapid reconstruction is not the availability of suitable equipment, but the industry’s ability to find it, trust it, and move it quickly. Regional platforms that have solved part of this problem domestically provide a working template for a more ambitious, internationally connected recommerce infrastructure. The question for IOCs, NOCs, and EPCs is no longer whether such platforms work, but how quickly they can be adapted and scaled to meet the reconstruction needs before new equipment orders become the only option.

Conclusion

The challenge of post-war reconstruction in the Middle East presents an opportunity to leverage the vast amount of idle inventory already in place. With new equipment taking 9 months to 5 years to arrive, traditional procurement methods will lead to longer outages, higher project costs, and threats to regional and global energy security. In contrast, surplus and used equipment can be obtained 84-92% faster and at 30-70% lower costs, establishing a way to speed up recovery and reduce capital costs.

To tap into this potential, oil companies and contractors need to change how they source equipment. The three approaches outlined - using equipment they already have, transacting with others, and buying from third parties - are not new ideas, but are already working in places like Canada, where online platforms like IronHub have shown that surplus equipment can be reliably reused and sold on a large scale. To make this work, companies need to be able to see what equipment is available, ensure the data is accurate, and give contractors secure access to certified used equipment. This can turn idle assets worth hundreds of billions into a valuable resource for reconstruction.

If companies act quickly to make these changes - by using online platforms to buy and sell equipment, measuring success by how quickly they can get back up and running, and connecting digital systems to surplus markets - they can rebuild damaged oil and gas infrastructure at a significantly accelerated pace. The war has shown that relying on traditional supply chains is not reliable, so the response should be to build a more resilient and circular system that uses online platforms as a primary source of critical equipment.

| A guest post by

|